Random Process and Linear Algebra: Unit III: Random Processes,,

Poisson Process

Continuous time Markov Chain

If X(t) represents the number of occurrences of a certain event in (0, t), then the discrete random process {X(t)} is called the Poisson process, provided that the following postulates are satisfied. (i) P[1 occurrence in (t, t+∆t)] = λ ∆t + 0 (∆t) (ii) P [0 occurrence in (t,t+t∆)] = 1 - λ ∆t + 0 (∆t) (iii) P [2 or more occurrences in (t, t+∆t)] = 0 (∆t) (iv) X(t) is independent of the number of occurrences of the event in any interval prior and after the interval (0, t). (v) The probability that the event occurs a specified number of times in (t0, t0+t) depends only on t, but not on to. Poisson process is not a stationary process, as its statistical properties (mean, autocorrelation, ...) are time dependent.

POISSON

PROCESS [Continuous time Markov Chain]

Definition : [A.U. May 1999, N/D 2010, CBT A/M

2011] [A.U Tvli A/M 2011, CBT N/D 2011]

If X(t) represents the

number of occurrences of a certain event in (0, t), then the discrete random

process {X(t)} is called the Poisson process, provided that the following

postulates are satisfied.

(i) P[1 occurrence in

(t, t+∆t)] = λ ∆t + 0 (∆t)

(ii) P [0 occurrence in

(t,t+t∆)] = 1 - λ ∆t + 0 (∆t)

(iii) P [2 or more

occurrences in (t, t+∆t)] = 0 (∆t)

(iv) X(t) is

independent of the number of occurrences of the event in any interval prior and

after the interval (0, t).

(v) The probability

that the event occurs a specified number of times in (t0, t0+t)

depends only on t, but not on to.

Poisson process is not

a stationary process, as its statistical properties (mean, autocorrelation,

...) are time dependent.

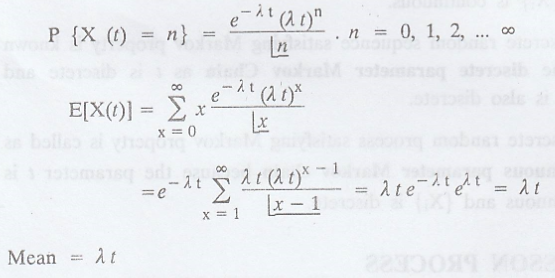

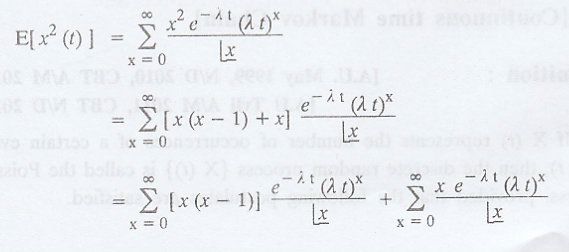

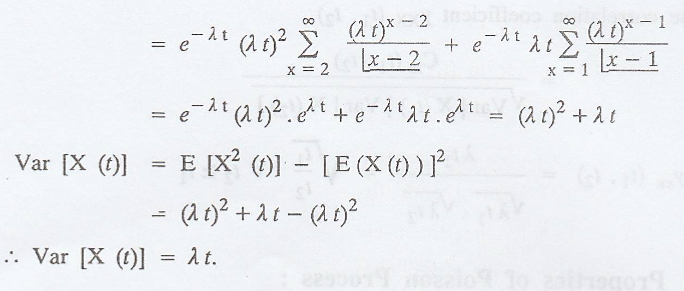

Mean and Variance of the Poisson Process: [A.U A/M 2003]

The probability

distribution of the Poisson process X(t) is given by,

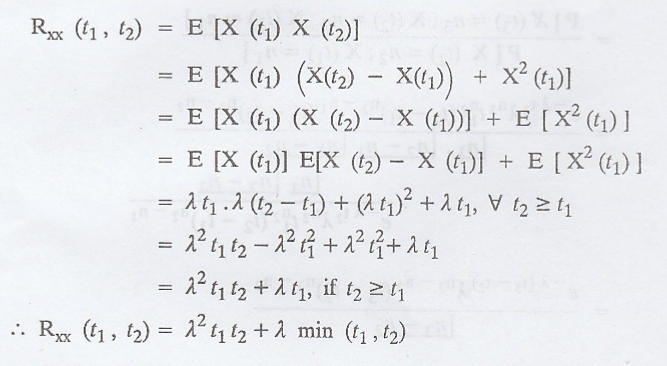

Autocorrelation of Poisson Random Process :

[A.U M/J 2014, A.U A/M

2015 (RP) R8, A.U M/J 2016 PQT R13] [A.U A/M 2018 R-13]

Let RXX (t1,

t2) is defined as the autocorrelation at time interval (t1,

t2).

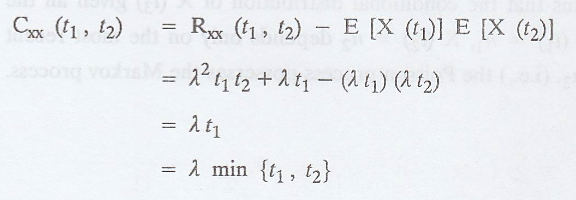

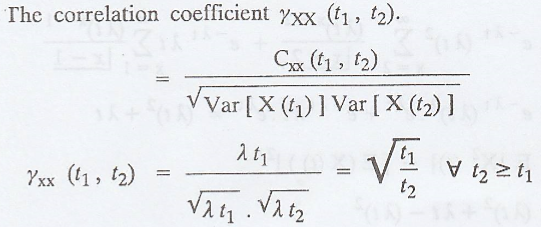

Relationship between mean, covariance and autocorrelation of Poisson

process

Properties of Poisson Process :

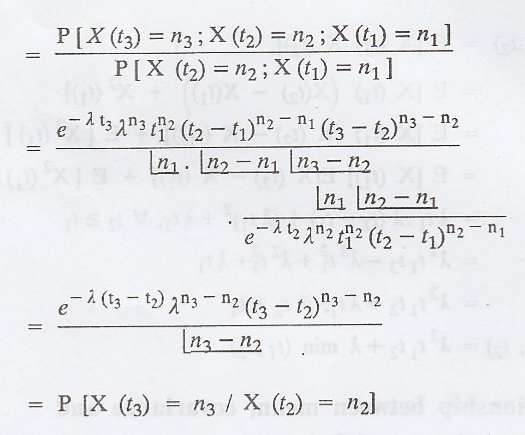

i. The Poisson process is a Markov process : [A.U M/J 2013] A.U. M.E. June 2010

[A.U M/J 2013, N/D 2013] [A.U A/M 2018 R-08]

Let us consider

This means that the

conditional distribution of X(t3) given all the past values X(t1)

= n1, X(t2) = n2 depends only on the most

recent value X(t2) = n2. (i.e.,) the Poisson process

possesses the Markov process.

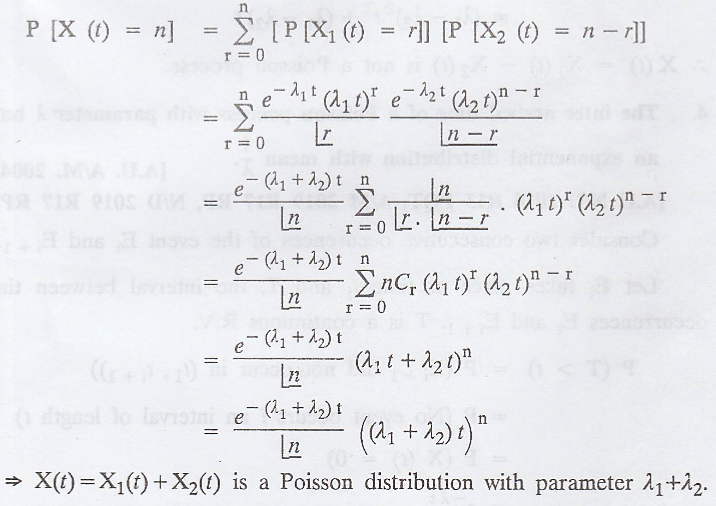

ii. The sum of two independent Poisson process is again a

Poisson process. (Additive property)

[OR]

If {X1(t)} and {X2(t)} are two independent

Poisson process with parameters λ1 and λ2 respectively,

show that the process {X1(t) + X2(t)} is also a Poisson

process.

[A.U. N/D 2006, N/D

2013, A/M 2014, A/M 2015 (RP) R-8] [A.U Trichy A/M 2010, CBT M/J 2010, Tvli M/J

2010] [A.U CBT A/M 2011, Trichy M/J 2011] [A.U M/J 2016 R13 PQT] [A.U N/D 2019

R-17 RP, PQT] [A.U A/M 2019 R17 PQT] [A.U A/M 2019 (R8) RP]

Proof :

Let X(t) = X1(t)

+ X2(t)

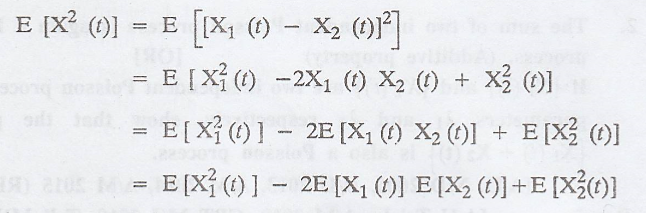

iii. The difference of two independent Poisson processes is not

a Poisson process. [A.U. A/M 2004, N/D 2003, A/M 2011]

[A.U Trichy A/M 2010, A.U Tvli M/J 2010, A.U Tvli. A/M 2011] [A.U M/J 2013]

[A.U M/J 2016 R13 PQT] [A.U N/D 2019 R17 PQT]

Proof :

Let X(t) = X1(t)

+ X2(t)

Then E [X(t)] = E[X1(t)

- X2(t)] = E[X1(t)] - E[X2(t)]

.'. X1(t)

and X2(t) are independent.

.'. X(t) = X1(t)

- X2(t) is not a Poisson process.

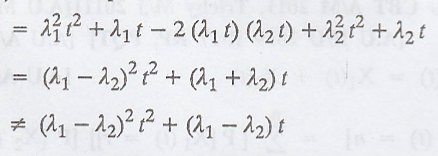

iv. The inter arrival time of a Poisson process with parameter λ

has an exponential distribution with mean 1/λ [A.U. A/M.

2004] [A.U N/D 2016 R13 PQT, A/M 2019 R17 RP, N/D 2019 R17 RP]

Proof:

Consider two

consecutive occurences of the event Ei and Ei+1.

Let Ei takes

place at time ti and T, the interval between the occurrences Ei

and Ei+1. T is a continuous R.V.

The c.d.f of T is given

by

The p.d.f of T is given

by f(t) = λe – λ t, t ≥ 0

This is a exponential

distribution with mean 1/λ

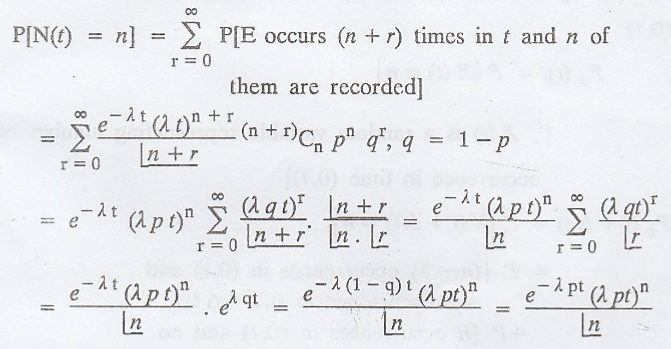

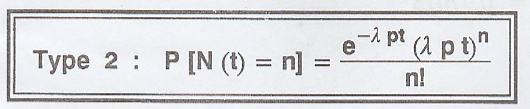

v. If the no. of occurrences of an event E in an interval of

length 't' is a process {X(t)} with parameter λt and if each occurrence of E

has a constant probability 'p' of being recorded and the recording are

independent of each other, then the number N(t) of the recorded occurrences in

t is also a Poisson process with parameter λp. [A.U. A/M.

2004]

=> N(t) is a Poisson

random process.

If {X(t)} is a Poisson process, prove that

Proof

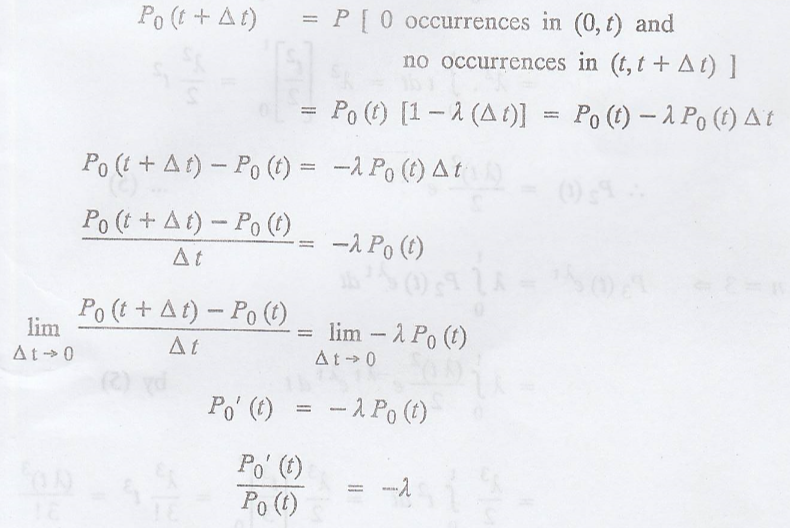

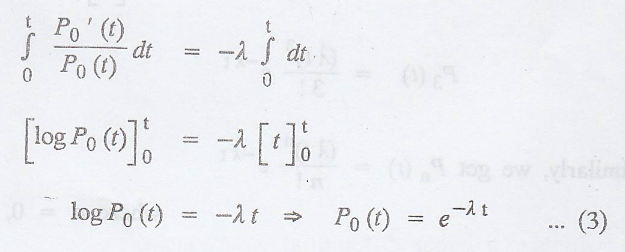

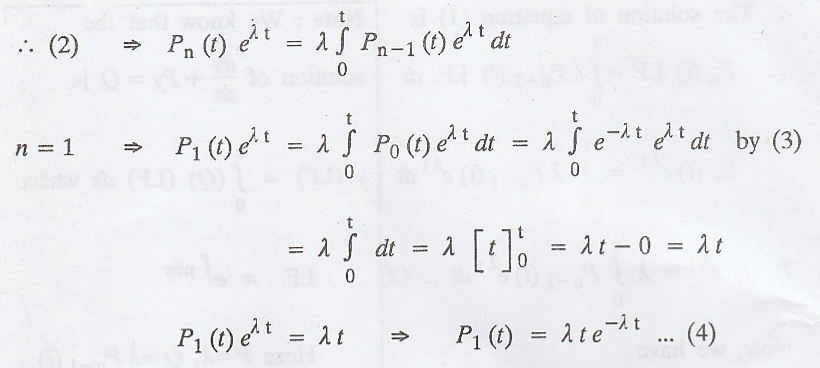

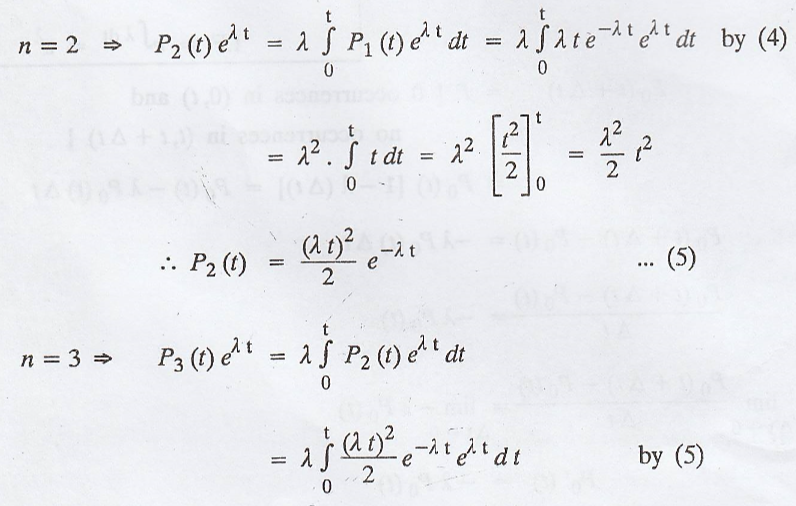

Derivation of the probability law (or probability function or

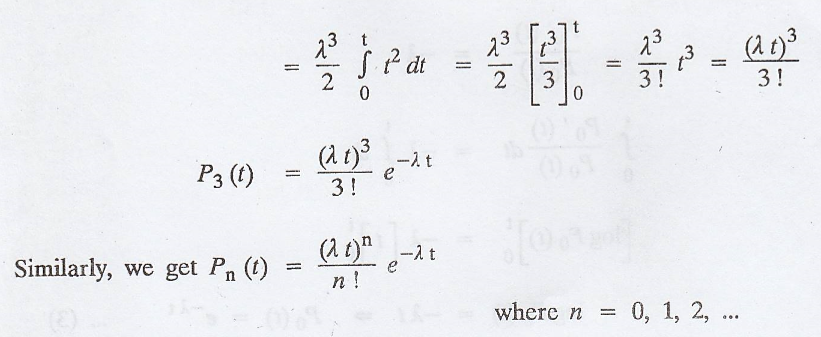

probability distribution) for the Poisson process X(t).

[A.U A/M 2011] [A.U N/D 2019 R17 PQT]

Let λ be the number of

occurrences of the event in unit time.

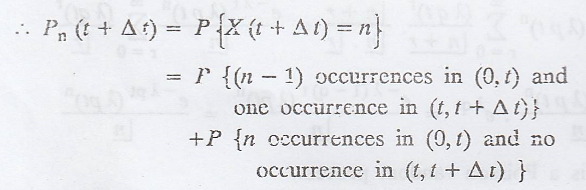

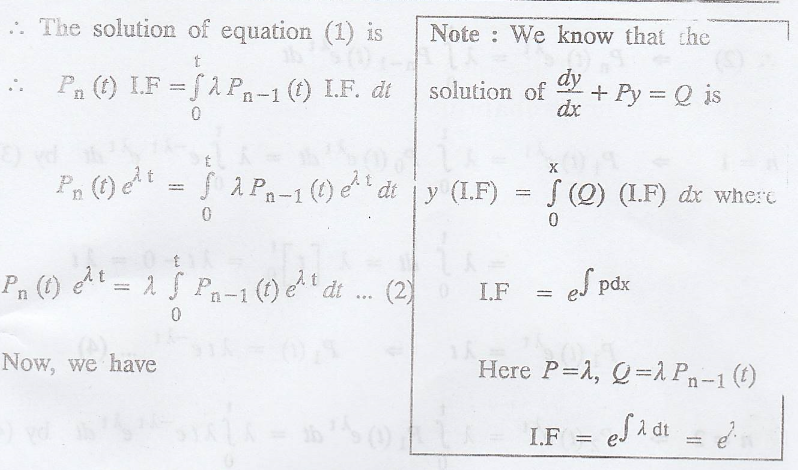

Let Pn(t)

represent the probability of n occurrences of the ever n (0,t)

['.' X(t) is a random

variable representing number of occurrence in time (0,t)]

[by the postulates of

Poisson process neglecting 0 (∆t)]

which is a linear

differential equation.

Example 3.6.1

If patients arrive at a

clinic according to Poisson process with mean rate of 2 per minute. Find the

probability that during a 1-minute interval, no patient arrives. [A.U A/M 2017

R-13 RP]

Solution

:

Let X(t) be the number

of patients arrive at a clinic in the time interval of t.

Given:

Mean rate, λ = 2 per

minute

Time interval, t = 1

per minute

No. of arrivals, n = 0

X(t) follows a Poisson

process, P[X(t) = n] = e – λ t (λt) n / n!

Example 3.6.2

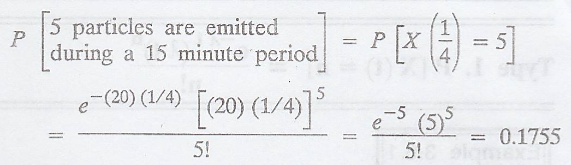

If particles are

emitted from a radio active source at the rate of 20 per hour, find the

probability that exactly 5 particles are emitted during a 15 minute period.

[A.U CBT A/M 2011]

Solution

:

Let X(t) be the number

of particles are emitted in the time interval of t.

Given:

Mean rate, λ = 20 per

hour

Time interval, t = 15

min = 15/60 hrs = 1/4 hrs.

No. of arrivals, n = 5

X(t) follows a Poisson

process, P[X(t) = n] = e – λ t (λt) n / n!

Example 3.6.3

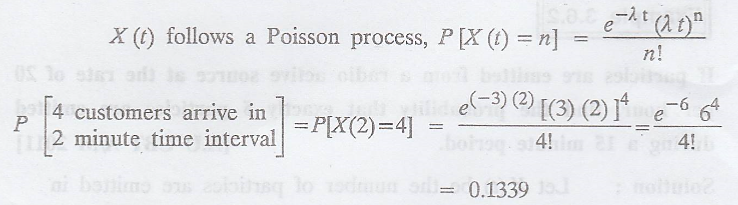

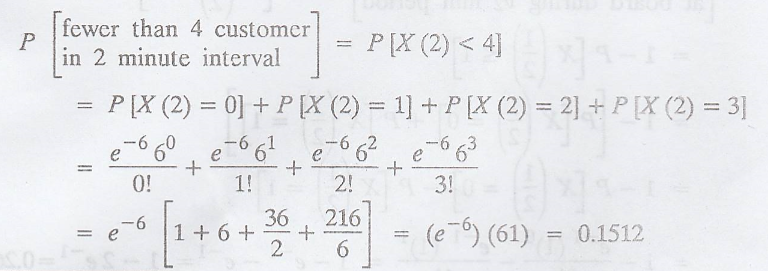

Suppose that customers

arrive at a bank according to a poisson process with a mean rate of 3 per

minute; find the probability that during a time interval of 2 min (i) exactly 4

customers arrive and (ii) more than 4 customers arrive. (iii) fewer than 4

customer in 2 minute interval. [A.U M/J 2009, CBT N/D 2011, M/J 2012, M/J 2013]

[A.U N/D 2013, A/M 2015 R-8, N/D 2015, R13 PQT] [A.U N/D 2015, R13 RP] [A.U A/M

2017 R-08]

Solution

:

Let X(t) be the number

of customers arrive at a bank in the time interval of t.

(i) Mean rate, λ = 3

per minute

Time interval, t = 2

per minute

No. of arrivals, n = 4

(ii) Mean rate, λ = 3

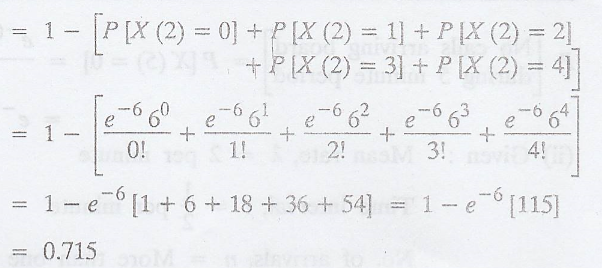

per minute

Time interval, t = 2

per minute

No. of arrivals, n =

more than 4.

P[more than 4 customers

in 2 min. interval]

= P[X(2) > 4] = 1 -

P[X(2) ≤ 4]

(iii) Mean rate, λ = 3

per minute

Time interval, t = 2

per minute

No. of arrivals, n =

fewer than 4

Example 3.6.4.

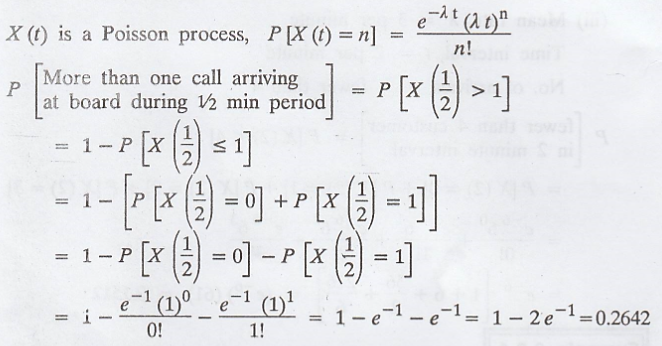

The number of telephone

calls arriving at a certain switch board within a time interval of length

(measured in minutes) is a Poisson process X(t) with parameter λ = 2. Find the

probability of (i) No telephone calls arriving at this switch board during a 5

minute period. (ii) More than one telephone call arriving at this switch board

during a given 1/2 minute period. [AU Model]

Solution

:

Let X(t) be the number

of calls arrive at a board in the time interval of t.

(i) Given: Mean rate, λ

= 2 per minute

Time interval, t = 5

per minute

No. of arrivals, n = 0

X(t) is a Poisson

process, P[X(t) = n] = e – λ t (λt) n / n!

(ii) Given: Mean rate,

λ = 2 per minute

Time interval, t = 1/2

per minute

No. of arrivals, n =

More than one call

Example 3.6.5

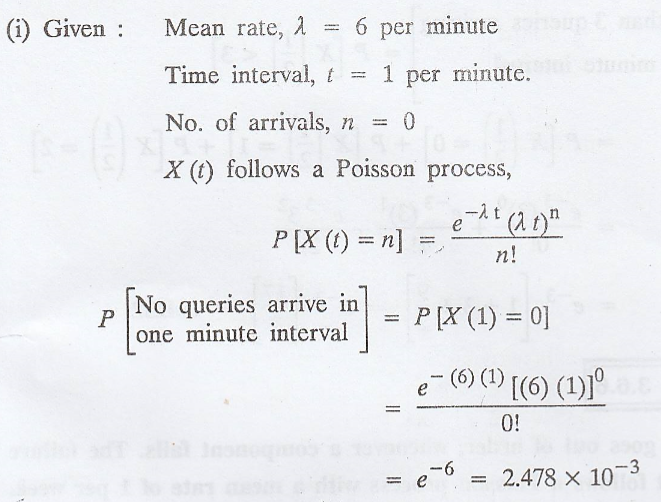

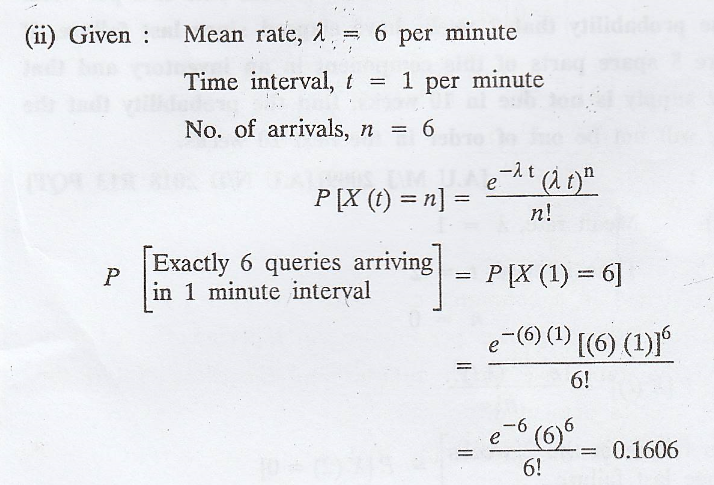

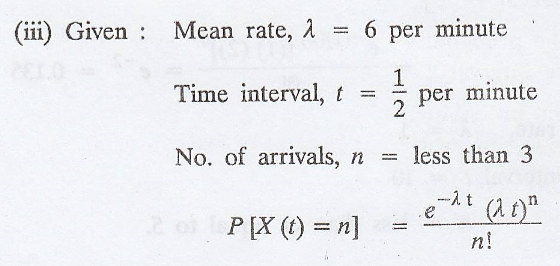

Queries presented in a

computer data base are following a Poisson process of rate λ = 6 queries per

minute. An experiment consists of monitoring the data base for m minutes and

recording N(m) the number of queries presented.

(1) What is the

probability that no queries arrive in one minute interval ?

(2) What is the probability

that exactly 6 queries arriving in one minute interval?

(3) What is the

probability of less than 3 queries arriving in a half minute interval ? [A.U.

M/J 2007]

Solution

:

Let N(m) (or) X(t) be the number of queries presented in m (or) t minutes.

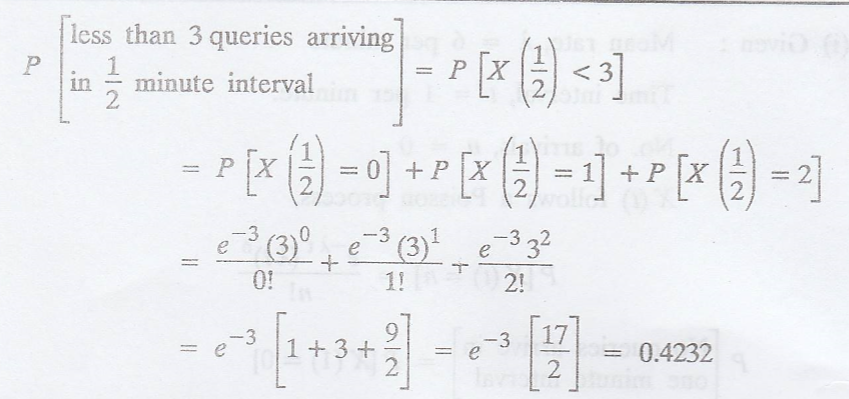

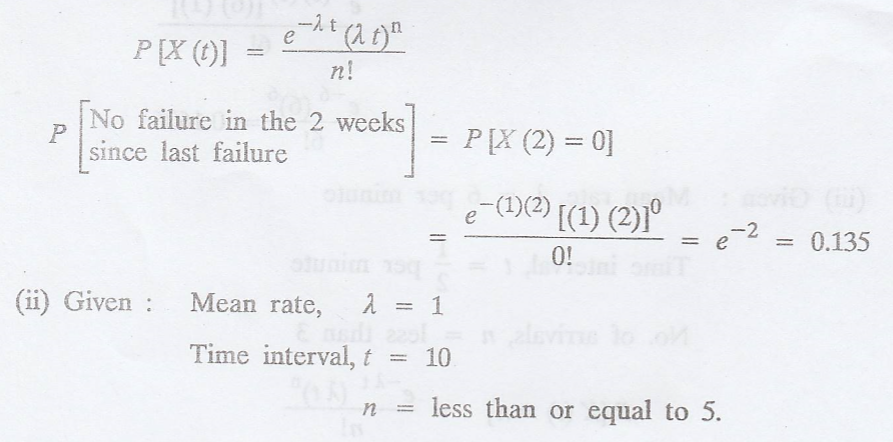

Example 3.6.6

A machine goes out of

order, whenever a component fails. The failure of this part follows a Poisson

process with a mean rate of 1 per week. Find the probability that 2 weeks have

elapsed since last failure. If there are 5 spare parts of this component in an

inventory and that the next supply is not due in 10 weeks, find the probability

that the machine will not be out of order in the next 10 weeks. [A.U M/J 2009]

[A.U N/D 2018 R13 PQT]

Solution

:

(i) Given:

Mean rate, λ = 1

Time interval, t = 2

n = 0

Example 3.6.7

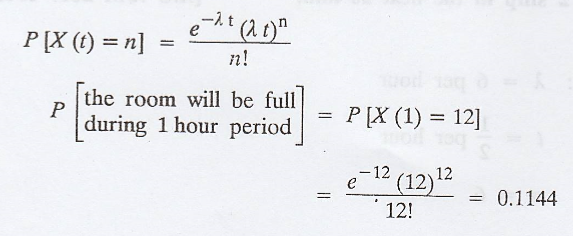

Patients arrive

randomly and independently at a doctor's consulting room from 8 a.m. at an

average rate of one in 5 min. The waiting room can hold 12 persons. What is the

probability that the room will be full when the doctor arrives at 9 a.m?

Solution

:

Let X(t) be the number

of patients arrive doctor's room in the time interval t.

Given: Mean rate, λ =

12 per hour

['.' 1 in 5 min ⇒ 12 in 60 min => 12

in 1 hour]

Time interval, t = 1

per hour

No. of arrivals, n = 12

Example 3.6.8

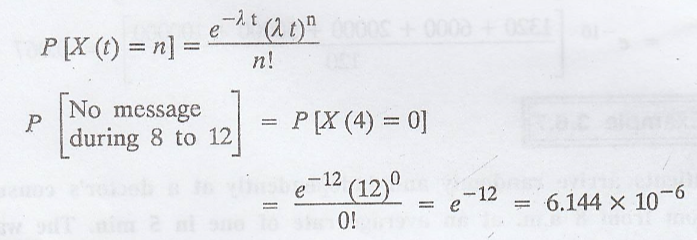

Messages arrive at a

telegraph office in accordance with the laws of a Poisson process with a mean

rate of 3 messages per hour. What is the probability that no message will have

arrived during the morning hours i.e., between 8 a.m. and 12 noon?

Solution

:

Given: Mean rate, λ = 3

per hour

Time arrival, t = 4 per

hour

Number of arrivals, n =

0

Example 3.6.9

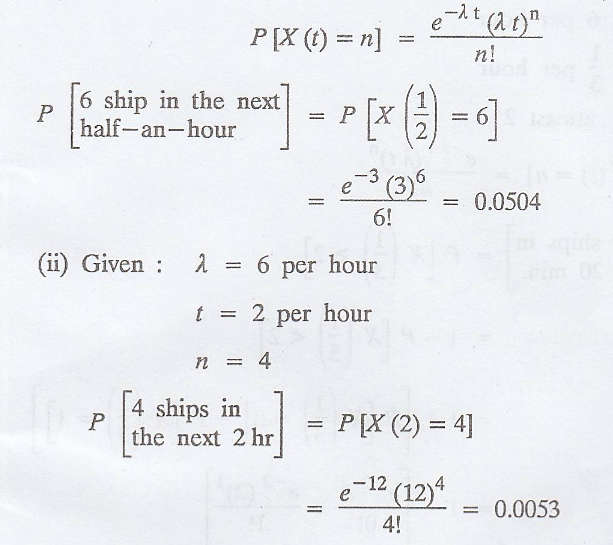

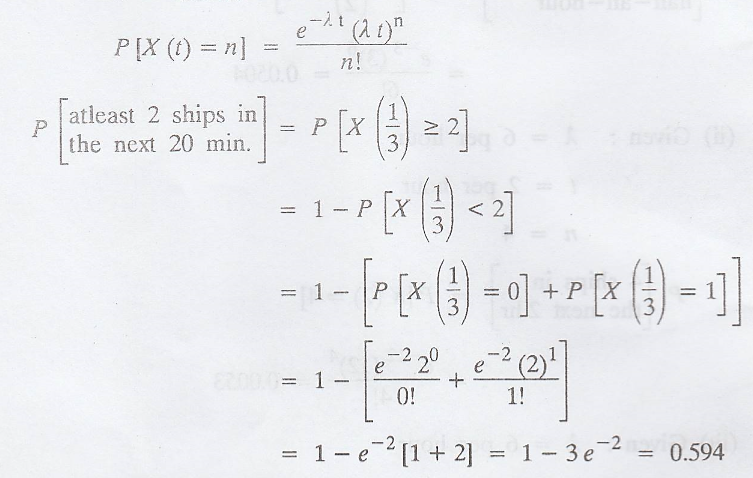

On the average, a

submarine on patrol sights 6 enemy ships per hour. Assuming that the number of

ships sighted in a given length of time is a Poisson variate, find the

probability of sighting

(i) 6 ships in the next

half-an-hour.

(ii) 4 ships in the

next 2h,

(iii) atleast 1 ship in

the next 15 min.

(iv) atleast 2 ship in

the next 20 min. [A.U A/M 2017 R-13]

Solution

:

(i) Given: λ = 6 per

hour

t = 1/2 per hour

n = 6

(iv) Given: λ = 6 per

hour

t = 1/3 per hour

n = atleast 2

Example 3.6.10

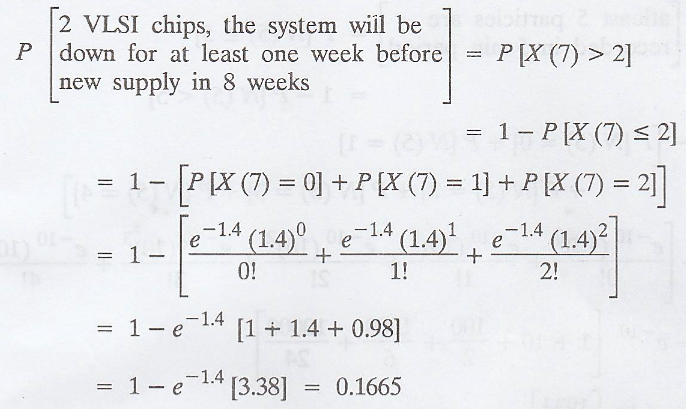

VLSI chips, essential

to the running of a computer system, fail in accordance with a Poisson

distribution with the rate of one chip in about 5 weeks. If there are two spare

chips on hand, and if a new supply will arrive in 8 weeks, what is the

probability that during the next 8 weeks the system will be down for a week or

more, owing to the lack of chips? [AU Nov. 2007]

Solution

:

Given: Mean rate, λ =

1/5

Time interval, t = 7

Number of arrivals, n =

greater than 2

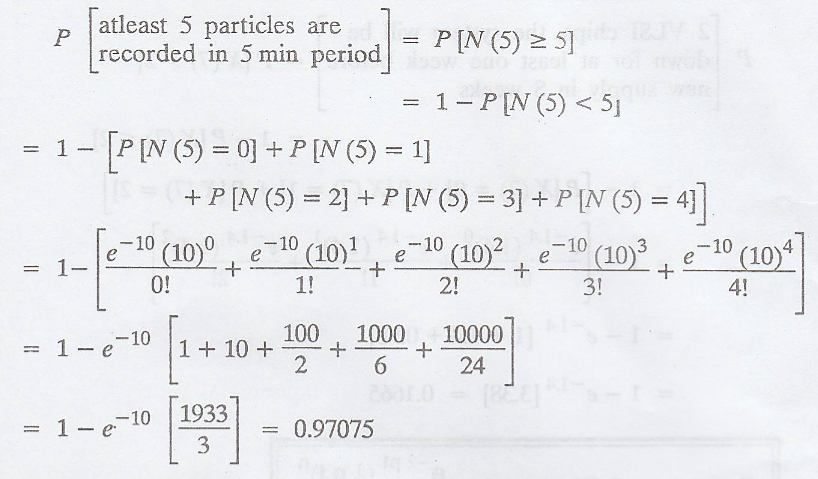

Example 3.6.11

A radio active source

emits particles at the rate of 6 per minute in a Poisson process. Each emitted

particle has a probability of 1/3 being recorded. Find the probability that

atleast 5 particles are recorded in a 5 minute-period. [A.U N/D 2018 R13 RP]

Solution

:

N(t) is a Poisson

process with parameter λp

Mean rate, λ = 6 per

minute

Event has a constant probability,

p = 1/3

Time interval, t = 5

per minute

Number of recorded, n =

5

λpt = (6) (1/3) (5) =

10

P[N(t)

= n] = e – λ t (λt) n / n!

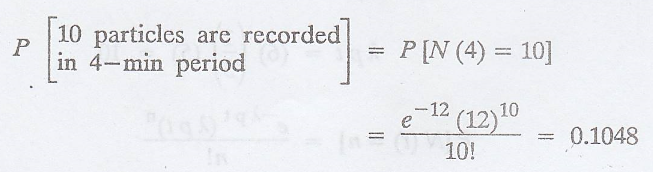

Example 3.6.12

A radioactive source

emits particles at a rate of 5 per minute in accordance with Poisson process.

Each particle emitted has a probability 0.6 of being recorded. Find the

probability that 10 particles are recorded in 4-min period. [A.U N/D 2014] [A.U

A/M 2019 R13 PQT]

Solution

:

N(t) is a Poisson

process with parameter λp

Mean rate, λ = 5 per

minute ho

Event has a probability

constant, p = 0.6

Time interval, t = 4

per minute

No. of recorded, n = 10

λpt = (5) (0.6) (4) =

12

P[N(t)

= n] = e – λ t (λt) n / n!

Type 3.

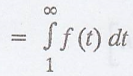

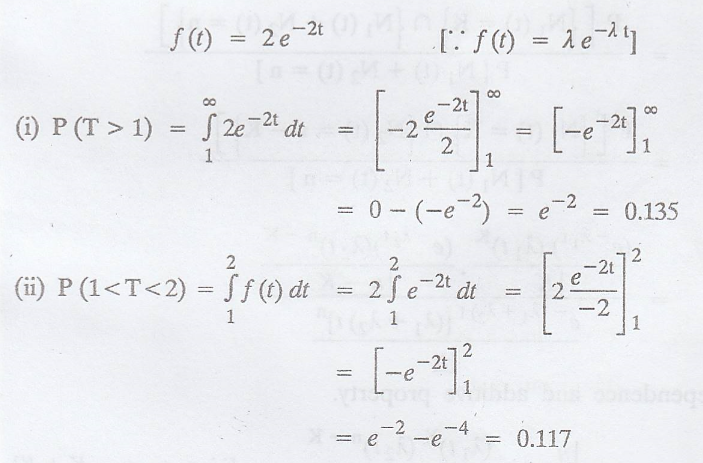

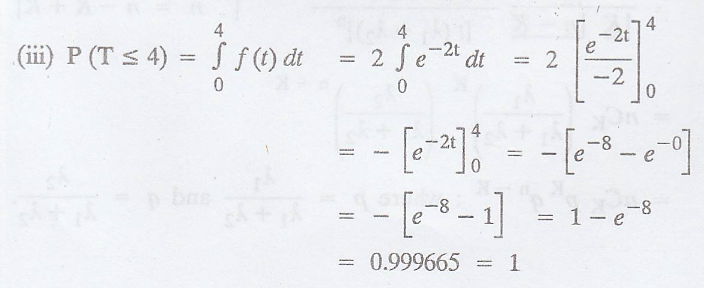

Example 3.6.13

If customers arrive at

a counter in accordance with a Poisson process with a mean rate of 2 per

minute, find the probability that the interval between 2 consecutive arrivals

is (i) more than 1 min, (ii) between 1 min. and 2 min. and (iii) 4 min. or

less. [A.U. 2006 N/D 2010, N/D 2011 M/J 2012]

Solution

:

By the property of

Poisson process, the interval T, between 2 consecutive arrivals follows an

exponential distribution with parameter (λ = 2)

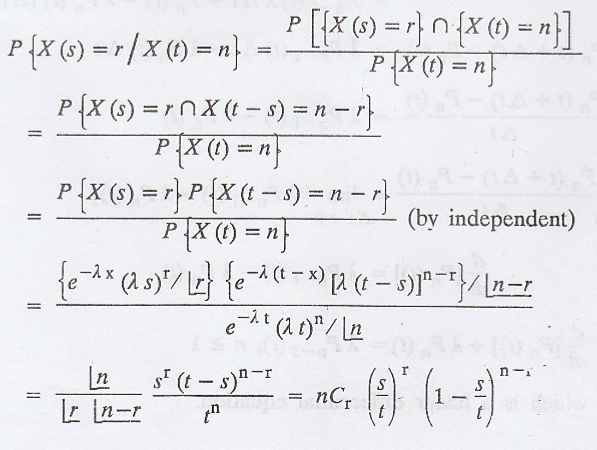

Example 3.6.14

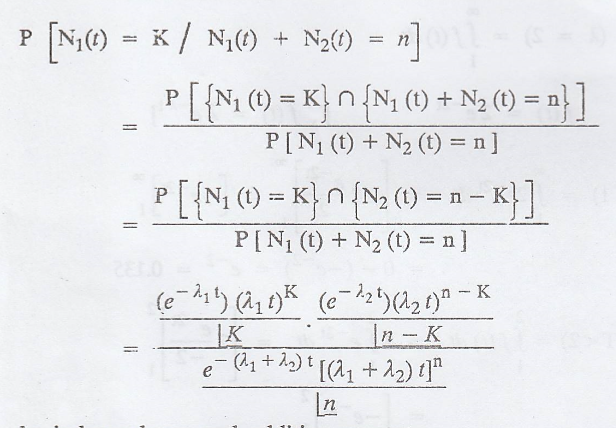

If {N1(t)}

and {N2(t)} are 2 independent Poisson process with parameters λ1

and λ2 respectively, Show that

[A.U N/D 2015 R-8, A.U

A/M 2018 R-8] [A.U A/M 2019 R17 RP]

Solution:

The required

conditional probability is

by independence and

additive property.

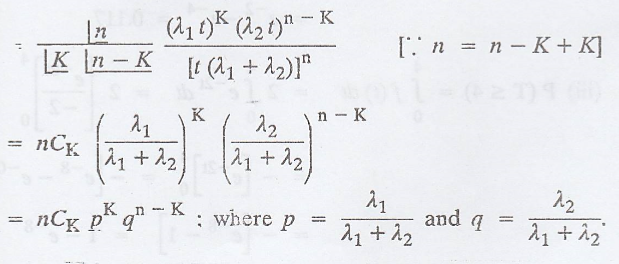

Example 3.6.15

If {X(t)} and {Y(t)}

are two independent Poisson processes, show that the conditional distribution

{X(t)} given {X(t) + Y(t)} is binomial. [A.U. N/D 2006]

Solution:

Let {X(t)} & {Y(t)}

be two independent Poisson processes with λ1t & λ2t

respectively. Hence {X(t) + Y(t)} is also Poisson process with parameter λ1t

+ λ2t

Example 3.6.16

Examine

whether the Poisson process X(t) given by the probability law P[N(t) = n] = e –

λ t (λt) n / n!, n = 0, 1, 2, ... is covariance stationary or

not. [A.U A/M 2005, A.U. N/D 2007] [A.U A/M 2019 (R17) RP]

Solution:

Given:

X(t) = P[N(t) = n] = e – λ t (λt) n / n!

We

know that X(t) is a Poisson distribution with parameter λt.

→ E[X(t)] = λt ≠ a

constant.

→ The Poisson process

is not a SSS process and not a WSS process.

→ The Poisson process

is not a covariance stationary.

EXERCISE 3.6

1. Assume that a

circuit has a IC whose time to failure is an exponentially distributed R.V with

expected life time of 3 months. If there are 10 spare IC's and time from

failure to replacement is zero, what is the probability that the circuit can be

kept operational for atleast 1 year? [Ans. 0.9972]

2. Suppose that

customers arrive at a counter independently from 2 different sources. Arrivals

occur in accordance with a Poisson process with mean rate of 6 per hour from

the first source and 4 per hour from the second source. Find the mean interval

between any 2 successive arrivals. [Ans. 6 minutes]

3. Assume that an

office switch board has 5 telephone lines and that starting at 8 A.M on Monday,

the time that a call arrives on each line is an exponential R.V with parameter

λ. Also assume that the calls arrive independently on the lines. Show that the

time of arrival of the first call (irrespective of which line it arrives on) is

exponential with parameter 5λ.

4. Passengers arrive at

a terminal for boarding the next bus. The times of their arrival are Poisson

with an average arrival rate of 1 per minute. The times of departure of each

bus are Poisson with an average departure rate of 2 per hour. Assume that the

capacity of the bus is large. Find the average number of passengers in (i) each

bus, (ii) the first bus leaves after 9 a.m. [Ans. 30, 60]

5. Students enter a

hall at a Poisson rate of λ = 1 per second. What is the expected time until the

eleventh student arrives? What is the probability that the elapsed time between

the eighteenth and nineteenth student arrivals exceed two seconds ? [Ans. 11

sec, 0.13]

6. The number of

typographical errors on a single page of a document is poisson distributed with

λ = 1. What is the probability that there is atleast one error on a page ?

[Ans. 0.633]

7. A hospital receives

an average of 3 emergency calls in a 10 minute interval. What is the

probability that there are atmost 3 emergency calls in 10 minutes interval.

[Ans. 0.647]

8. A hard disk fails in

a computer system and it follows a Poisson distribution with mean rate of 1 per

week. Find the probability that 2 weeks have elapsed since last failure. If we

have 5 extra hard disks and the next supply is not due in 10 weeks, find the

probability that the machine will not be out of order in the next 10 weeks.

[Ans. 0.135, 0.068] [AU June 2007] [A.U N/D 2017 (RP) R-13]

9. A fisherman catches

fish at a Poisson rate of 2 per hour from a large pond with lots of fish. If he

starts fishing at 10.00 a.m., What is the probability that he catches one fish

by 10.30 a.m. and three fish by noon? [Ans. 0.082] [AU April 2004] [A.U A/M

2017 (RP) R-13]

Random Process and Linear Algebra: Unit III: Random Processes,, : Tag: : Continuous time Markov Chain - Poisson Process

Related Topics

Related Subjects

Random Process and Linear Algebra

MA3355 - M3 - 3rd Semester - ECE Dept - 2021 Regulation | 3rd Semester ECE Dept 2021 Regulation